As of midday today, it remains unclear whether or not the Federal Reserve will raise interest rates on Thursday. If it does, it will be the first time rates have been raised since June 2006. Why is this even a matter of debate?

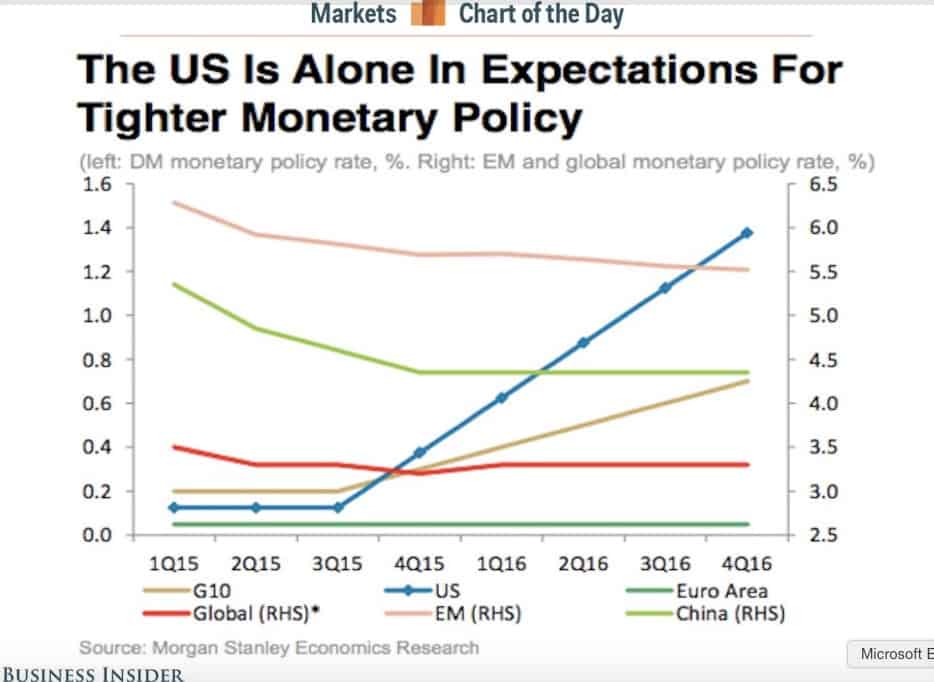

For one thing, it appears that the Fed will be acting alone if it raises rates. This chart shows just how much an outlier the U.S. has become, simply because there is an expectation of tighter monetary policy in the near future:

As Business Insider notes, right now “it's a world of easy monetary policy, meaning low interest rates and, in the case of the European Central Bank and Bank of Japan, outright asset purchases.”

It's a world of easy monetary policy ... everywhere, that is, except, the United States. And yet, if the Fed is to be an outlier among central banks, it might be expected to be more concerned about jobs, wages and inequality than its peers – not less. That's because, unlike other central banks, it has a dual mandate to manage both monetary policy and unemployment.

To be clear, many observers believe the Fed will not raise rates this week. But many of them feel it will do so in the coming months, perhaps in March. Public statements from Fed officials have certainly left the impression that a rate increase could be imminent.

If it does raise rates Thursday, the Fed would be rejecting the advice of many leading economists. Nobel Prize winner Joseph Stiglitz makes a compelling case against such a move in a Guardian essay headlined “Federal Reserve needs to worry about inequality, not inflation.” Stiglitz writes:

“There is strong evidence that economies perform better with a tight labour market and, as the International Monetary Fund (IMF) has shown, lower inequality (and the former typically leads to the latter).”

Despite the good topline jobs numbers, there are a number of fundamental weaknesses in employment, including minority employment and overall participation in the workforce. Stiglitz details those weaknesses – weaknesses which would be made worse by an increase in interest rates. Wages would also suffer.

Stiglitz explains:

“If the Fed focuses excessively on inflation, it worsens inequality, which in turn worsens overall economic performance. Wages falter during recessions; if the Fed then raises interest rates every time there is a sign of wage growth, workers’ share will be ratcheted down – never recovering what was lost in the downturn.”

Two of President Obama’s economic advisors, Lawrence Summers and Gene Sperling, have also weighed in against raising rates this month.

What about the arguments for raising rates? As economist Brad DeLong writes, “The arguments for raising interest rates right now are of appallingly low-quality.” DeLong also suggests that “to establish credibility that its 2%/year inflation target is an average, and not a ceiling, (the Fed) needs to overshoot it for a period of time in the near future.”

So why is a rate increase even a possibility?

One clue can be found in Stiglitz’ observation that “the argument for raising interest rates focuses not on the wellbeing of workers, but that of the financiers.” Despite the fact that it’s a publicly created institution, bankers and other private interests are very involved in the governance of the Federal Reserve.

To the Fed’s credit, it is reportedly taking the needs of the labor market into consideration to a much greater degree than it has in the past. Fed Chair Janet Yellen appears to be more deeply committed to its dual mandate than her immediate predecessors. But many voices within the Fed, including Vice Chair Stanley Fischer, appear to be pushing for an increase.

Rate increases are appropriate when the economy is overheating, which is not the experience of most Americans today. And recent moves to counter inflation have been misguided. In fact, as Neil Irwin notes, “since the global financial crisis, when major central banks have erred, it has been overwhelmingly — perhaps exclusively — in the direction of excessive fear of inflation and complacency about growth.”

In other words, central bankers have been trying to fix the wrong problem. If the Fed raises rates tomorrow, it will be making the same mistake.

The Fed's answer is expected Thursday afternoon, but the surprise is that there's any question at all what it will do. That suggests that our economic debate is not yet grounded in economic reality, at least as most Americans experience it.