There was great economic news on Monday – for somebody.

Monday morning the stock market passed another historic milestone, as the S&P 500 composite index briefly passed the 2,000 mark before ending the day on a record-breaking high. That barrier had symbolic value for many investors, although perhaps not as much as the once-unimaginable goal of seeing the Dow Jones Industrial Average reach the 10,000 mark. A money manager in the go-go nineties once described that figure as “Mount Dow’s summit,” and so it was.

Once upon a time, investors could only dream of reaching that lofty Shangri-La.

But reach it they did. The Dow reached the 10,000 mark in 1999. Then it passed the 15,000 peak, in May of last year. That was well above its levels before the financial crisis, thanks to a Wall Street bailout that supercharged the stock market while others were left in the dust. As of this writing the S&P 500 is 1997.92, while the Dow closed today at a once-inconceivable 17,076.87.

No wonder the market’s hot. Corporate profits are soaring, and they’re expected to stay that way. “Based on the analysts' forecasts of S&P 500 companies,” writes Sam Ro in Business Insider, “… profit margins will average 9.3% for (this) year and then jump to 10.0% in 2015.”

There's no doubt about it: In some corners of the nation, life is sweet. But out beyond Washington and Wall Street and the Hamptons, out in the world where most Americans live, things aren’t quite as rosy. Floyd Norris of the New York Times described the economic landscape rather succinctly last April:

“Corporate profits are at their highest level in at least 85 years. Employee compensation is at the lowest level in 65 years.”

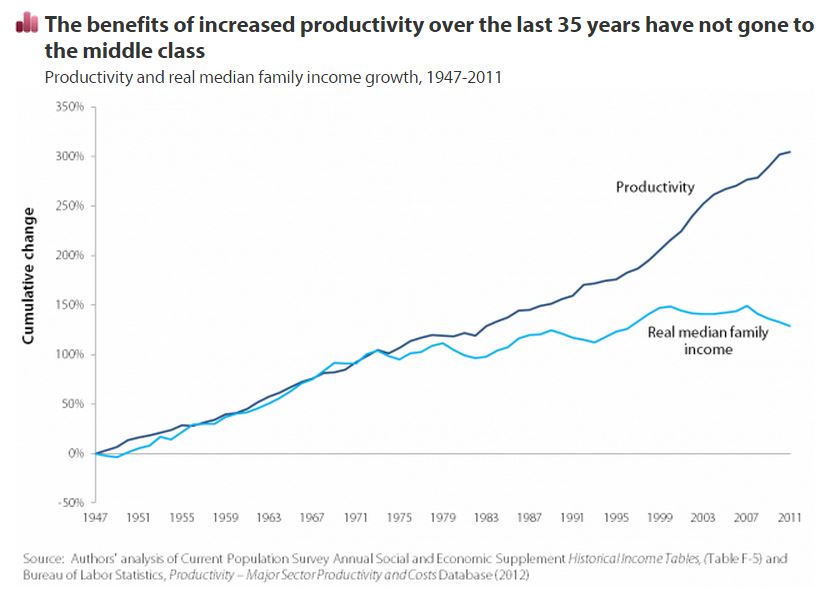

Norris notes that corporate profits reached a record-high 10 percent of GDP last year, while wages fell to a record-low 42.5 percent. By contrast, that figure was 49 percent in 2001. But while recent wealth shifts have been dramatic, these figures reflect much longer-term trends. For 30 years, during this country’s greatest economic boom, wages kept pace with increases in productivity:

Source: EPI

That ended in the mid-1970s. (Coincidentally or not, 1975 was also one of the first years in which wages fell to less than 50 percent of the GDP.)

Wage stagnation isn’t our only problem, of course. Unemployment figures remain troublingly high. Labor force participation is at historically low levels, leading even the historically conservative International Monetary Fund to call for policy intervention. Millions of people who want to work full time can only find part-time jobs. Job creation is lagging far behind what is needed to fully recover from the recession and keep pace with population growth.

The results continue to be devastating, especially for young people and minority communities. Continued weakness in the job market also contributes to stagnant wages by reducing competition for workers.

Then there’s poverty, a national tragedy few politicians seem willing to discuss. In 2012 the Census Bureau reported that 16 percent of the U.S. population was impoverished, including nearly one child in five. Last year, a UNICEF report showed that the United States has the second-highest child poverty rate in the developed world, outperforming only Romania.

Given these stunning and shameful disparities, it no longer makes sense to talk about “the U.S. economy.” We need to start thinking about our nation’s “economies,” of which there are at least two. There is the one that is inhabited by corporations, the wealthy, and the investor class. Call that one the “elite economy.” Then there’s the other economy, the one where most of us live. That's an economy under siege, an economy badly in need of advocates and defenders. This struggling economy isn’t a natural phenomenon, but is the result of conscious policy choices made by our nation's leaders.

What can be said about a political process that so faithfully executes the wishes of the wealthy and powerful at everyone else's expense? The ever-widening gulf between our two economies reflects a breakdown in our democracy – or, rather, a corruption of it on behalf of special interests. That’s reflected in our political elites’ continued insistence on job-killing spending curbs, despite the fact that the budget deficit fell by 24 percent last year – an “elite economy” concern – while jobs and wages continue to be a kitchen-table crisis for much of the country.

A recent Princeton study by Martin Gilens and Benjamin Page concluded that “economic elites and organized groups representing business interests have substantial independent impacts on U.S. government policy, while average citizens and mass-based interest groups have little or no independent influence.”

With their research, Gilens and Page confirmed something most Americans already understood instinctively: Our political system serves the few at the expense of the many. That's reflected in our economic data. On Monday we reached yet another stock-market milestone, while the economic gains that would affect most people's lives remain largely unrealized.

Reclaiming our democracy is one of the great challenges of our time. So is the task of making our divided economy whole once again. These challenges are interconnected, and they are urgent. They may seem daunting, but we have the knowledge and the resources to meet them and overcome them if we so choose.

We know what to do. All we need is the political will.