This piece by Aaron Carroll explains in full detail why raising the Medicare age is daft (and cruel):

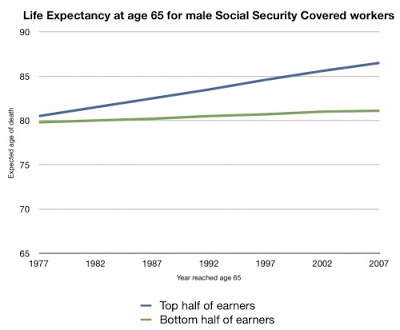

What you’re seeing is life expectancy at age 65 broken out in to the top half of earners and the bottom half of earners, from 1977 to 2007. I got these data from a study that appeared in Social Security Bulletin in 2007. The paper was entitled, “Trends in Mortality Differentials and Life Expectancy for Male Social Security-Covered Workers, by Socioeconomic Status.” We know that average life expectancy went up less than 5 years overall in this period. But what’s somewhat stunning is how much of a disparity there is in these gains. The top half of earners gained more than 5 years of life at age 65. The bottom half of earners, though, gained less than a year.

If you raise the age of eligibility by two years, then you are taking away more years of Medicare than half the country gained in longer life. Moreover, we’ve already taken away these people’s Social Security. The Greenspan Commission in the early 1980s made it so that the retirement age is already 66. It’s scheduled to rise to 67. So those at the bottom half of the socioeconomic ladder have already lost more years of Social Security than they’ve gained in years of life life expectancy at 65.

Sure, in a perfect world poor young seniors could get Medicaid if we take away their Medicare. That is, of course, if their state accepts the Medicaid expansion. Many haven’t. Less poor young seniors can go to the exchanges, I suppose. But if you’re a 65 year old widow and you make $46,100 a year in a high cost area, then your premium will be over $12,000 for your insurance. And you could owe another $6250 in out-of-pocket costs if you get sick. Tell me again how that person won’t miss her Medicare.

(He also explains is simple language why this whole " raised life expectancy" trope is nonsense to begin with. It pertains to life expectancy at birth not at the age of retirement. The designers of social security and medicare understood this even if nobody else seems to.)

So, we know that raising the Medicare age is a bad idea. How about the other very "clever" idea floating around these discussions: changing the accounting formula to cut benefits across all federal programs?

Here's the answer from Social Security Works:

Some politicians in Washington are preparing to cut your Social Security COLA for good--even after two years without getting a COLA. This COLA cut has an obscure name: chained-CPI. But it would do real damage by changing the formula used to calculate the COLA. Here's what you need to know about it:

It's a benefit cut. It's not some minor technical change to the COLA. It's a real cut to the benefits you have earned every year into the future.

It cuts benefits more with every passing year. After 10 years, your benefits would be cut by about $500 a year for the average retiree. After 20 years, your benefits would be cut by about $1,000 a year.

It hits today's Social Security beneficiaries. Politicians like to say that their cuts to Social Security will not affect those getting benefits today. Wrong! Switching to the chained-CPI would hit all current beneficiaries.

We need a higher COLA, not a lower one. The current COLA is not large enough--it does not adequately account for large health care cost increases faced by seniors and people with disabilities.

And it's not just social security. It's veterans and military retiree benefits, disability payments, federal worker pensions, anything the federal government funds.

Here's the thing, once again: all of this is unnecessary. The deficit caused by Bush's tax cuts, wars and recession will be largely mitigated by reinstatement of the upper income taxes, drawdown of the wars, growth(duh!) and, most importantly, controlling health care costs, the best method for which would have been expanding Medicare to cover everyone. We don't need to make this "clever" accounting change that will result in elderly and disabled people suffering. We can get serious about a rational national security policy, controlling health care costs, and espurring conomic growth and stop listening to the disaster capitalists who are intent upon using this window of opportunity to cut the programs they hate, whether the economy is good or bad. (Hell, we could even raise the top income tax rate above the Clinton levels, at least for those making a million dollars a year. These people have been making out like bandits and surely won't miss the money.)

If you know any veterans or military retirees, you might want to pass this fact sheet along to them. They tend to get testy when their promised benefits are threatened. They are a constituency worth organizing against this.